I hope everyone is having a nice weekend. The big news was the SCOTUS overruling the White House on IEEPA tariffs. He is already moving to other statutes, and we will assess the state of tariffs. The other notable development was FOMC minutes opening the right tail, as they did in March 1999.

In terms of data, we get factory orders tomorrow. On Tuesday we get Redbook, Case Schiller, Richmond Fed and Consumer Confidence. Wednesday has just MBS apps. Thursday has claims and KC Fed. Friday has PPI and Chicago Fed and is month end.

If you have not had a chance to read my Canada update, see it here: Carney's Gamble .

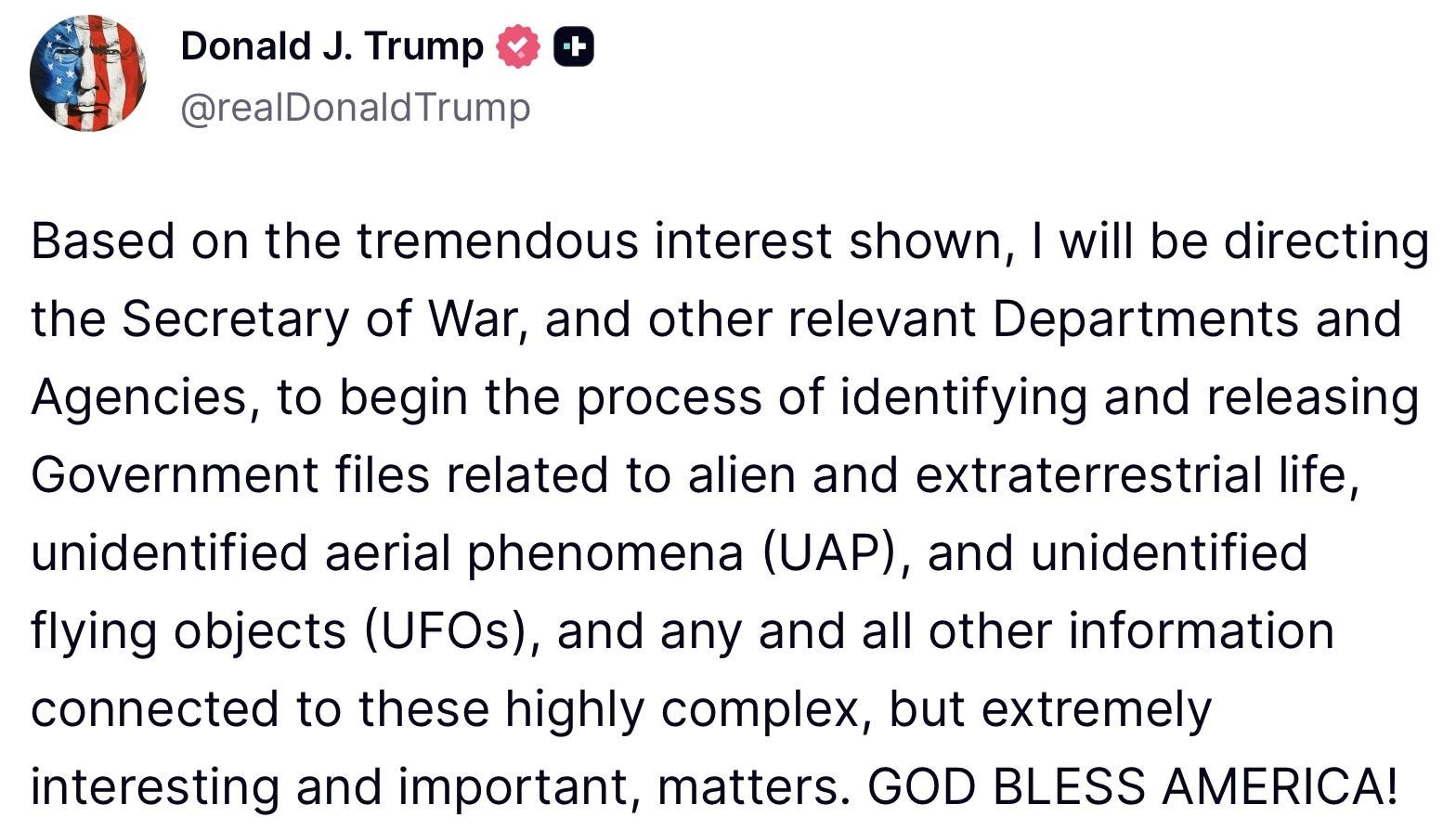

Oh, and we may finally get UFO disclosure. What a week!

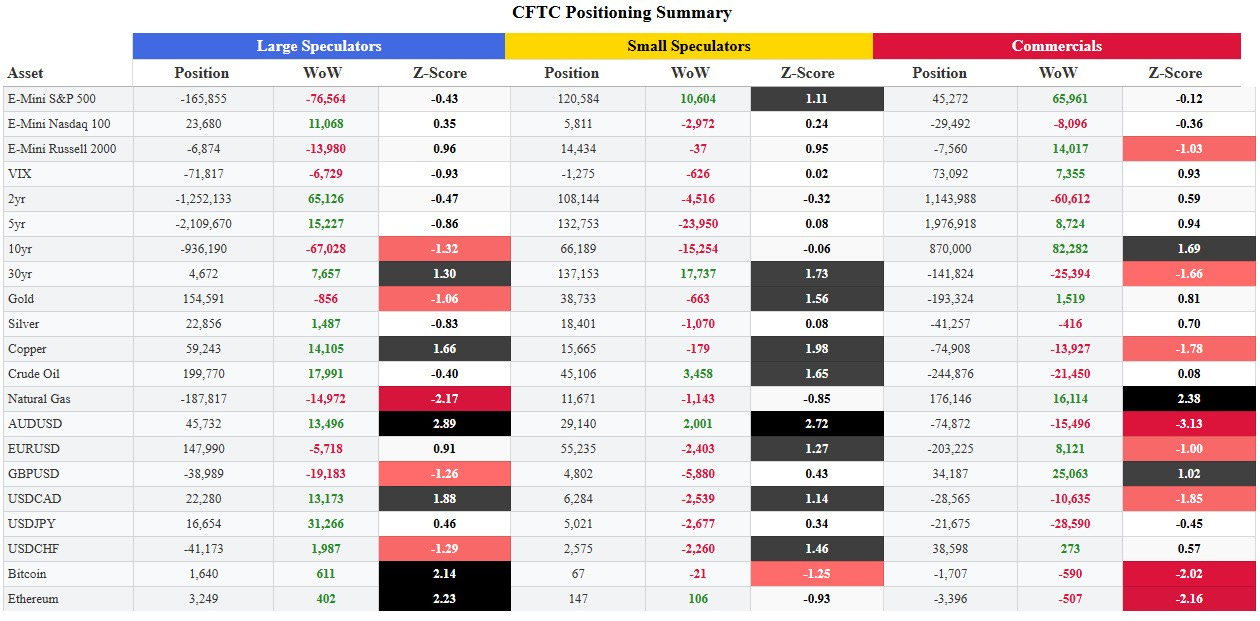

Positioning Summary and weekly changes is below.

Let’s dig in.

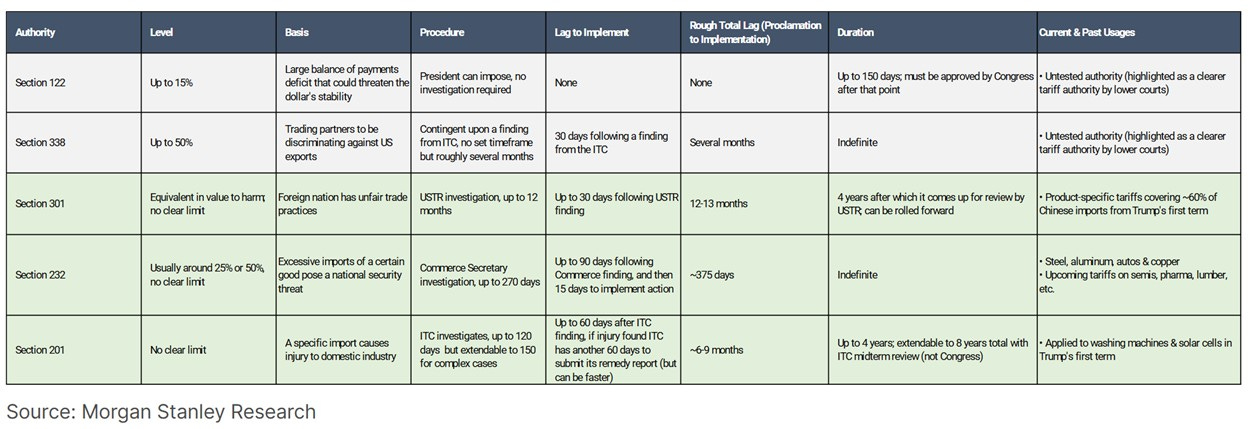

SCOTUS shut down the IEEPA tariffs. The key question surrounds whether the admin will be forced to refund about 150-200BN in tariffs. If so, that would raise the deficit and be more stimulus. Trump has plenty of other authorities to turn to, and the plan as of now is to do a global tariff of 15% for up to 150 days using Section 122, while starting the investigations to more lasting statutes like 301. There are a number of implications. For example, if there are refunds, it will likely be a corporate windfall as there is no way they will reduce prices for consumers to match their refunds. Secondly, will this tear up prior trade deals that had an effective tariff rate of 10%, and/or will countries seek to retaliate?

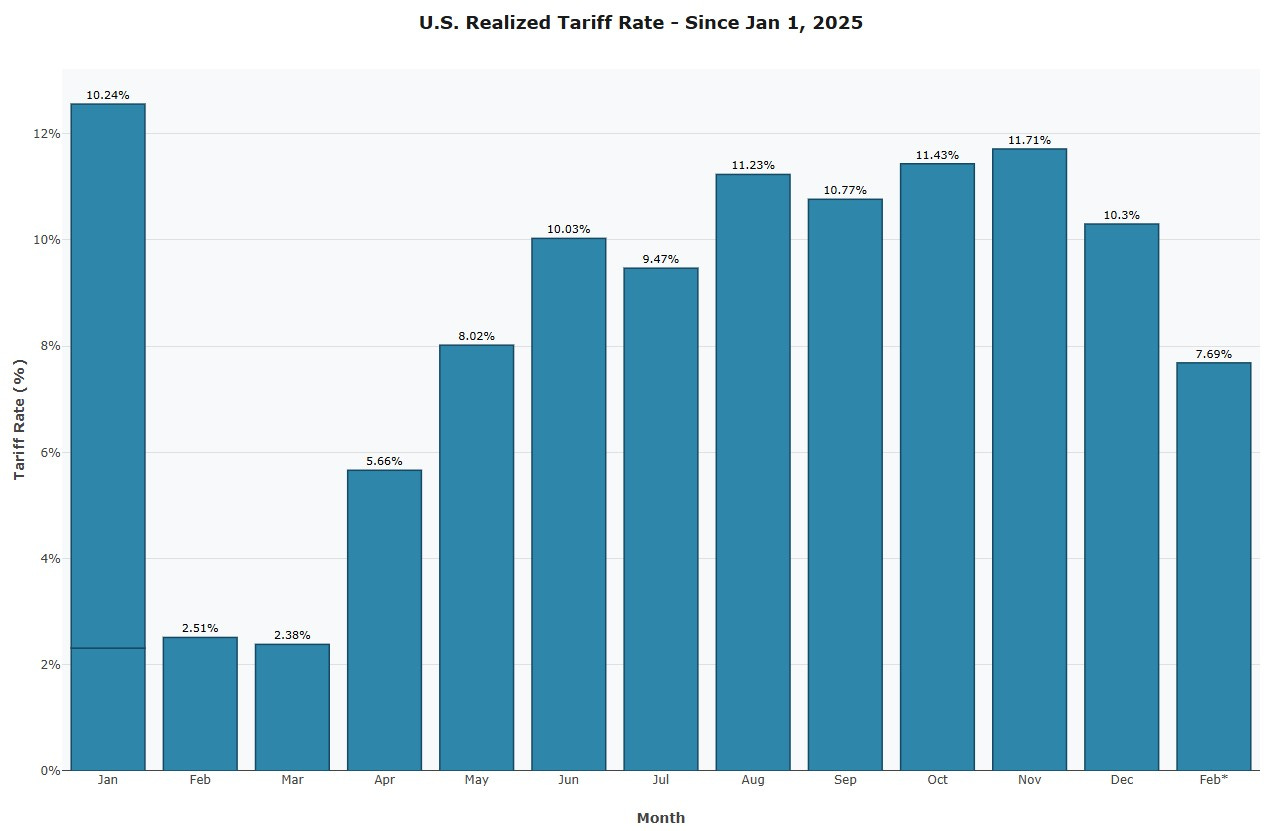

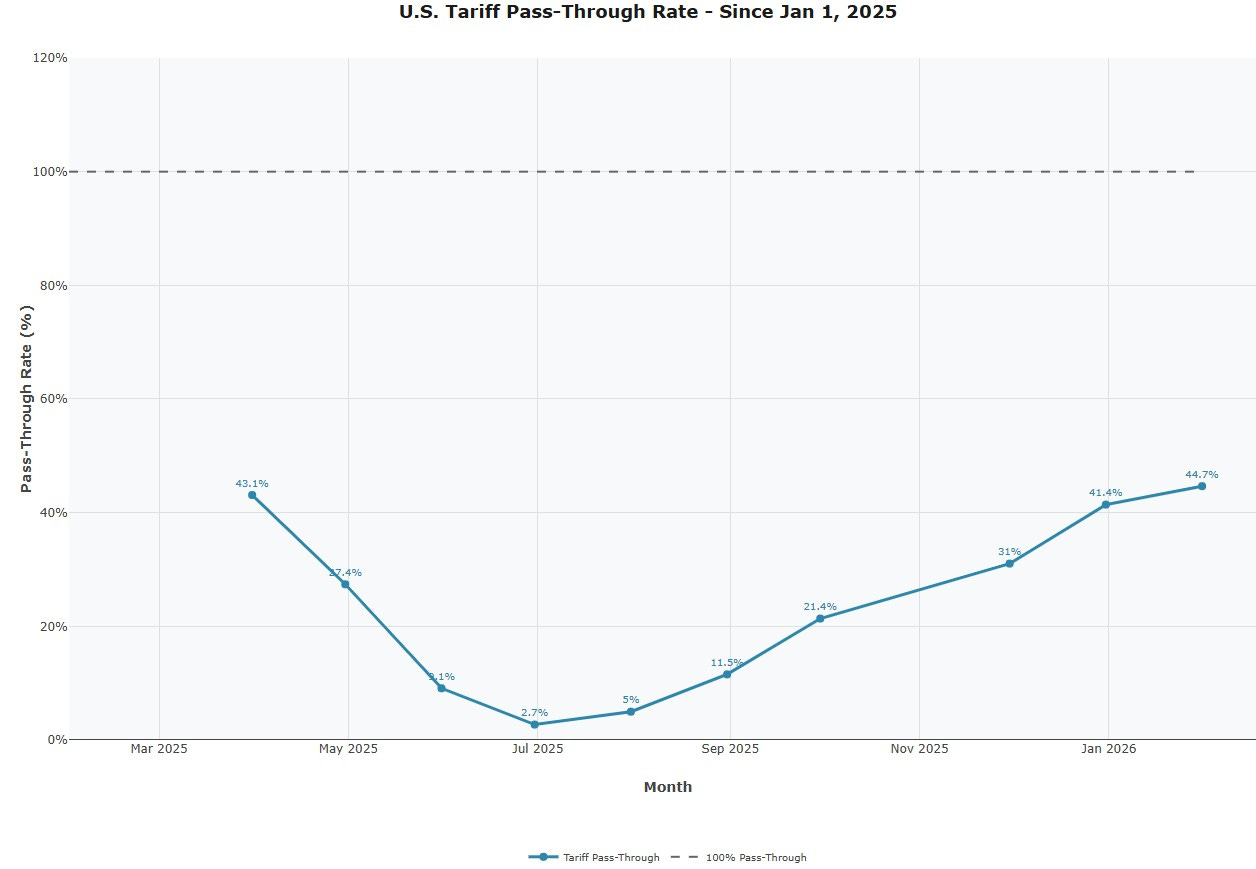

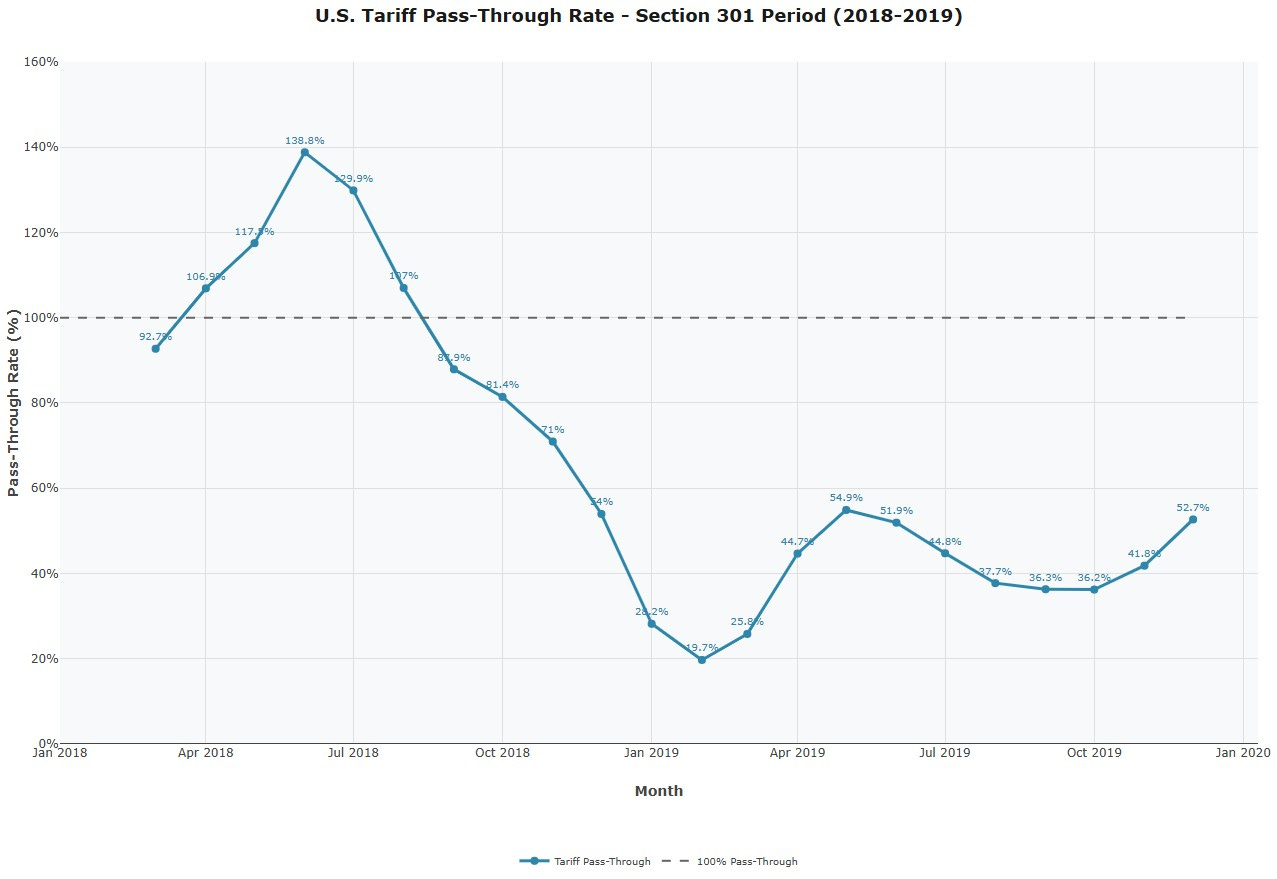

In looking at the state of tariffs, they have barely kicked in yet and are nowhere near max impact. Prior to this ruling, the effective tariff rate was about 18%, but the realized tariff rate has been in the 10-12% range for months. Secondly, the tariff pass through rate has been gradually rising since July last year and sits at 45%. In 2018, this was 80-90%. This changed when the economy slowed in Q4 and it declined to lower levels, before bouncing a bit in 2019.

Thus, I plugged a lower tariff rate of 15% into my Gordon Triangle model to simulate the impact on inflation. This model has a lot of assumptions and is not perfect (none are) but captures the supply side destruction impact that I believe is the key and missed by consensus. I should caution that with Core CPI distorted at 2.6% versus its true run rate of 3%, the starting point is thus lower and the ramp is more rapid than it is likely to be. However, the point remains, inflation will likely move up, then plateau at a level much higher than people expect if my assumption of a 10% permanent supply destruction holds.