I hope everyone is having a nice Memorial Day weekend. Before we jump in to the coming week, it is important to say thank you to the men and women who serve and have served to protect our freedoms.

A couple housekeeping notes. I had the pleasure of jumping onto the On the Margin Podcast last Wednesday. Ironically, one of the topics discussed was the fact that the 10y is too low, and has contributed to persistently loose financial conditions. Andy Constan released a note publicly on this topic that I find to be a really good summary of the dance between the Fed and Treasury that has prevented term premiums from properly expanding. Check out his note Fear is the policy stance.

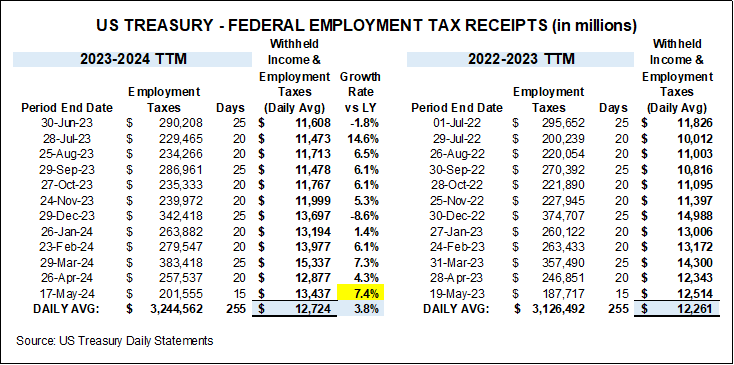

We have very little in terms of data releases this week, with GDP on Thursday and PCE on Friday, which coincides with month end. Most notable events last week were the Fed minutes , where it was confirmed that “various” members discussed rate hikes, as well as PMI and Jobless claims data that beat. While everyone seems to be looking for a slowdown, I have been making the case that it is unlikely for an income driven economy such as the US to simply fall off a cliff from one month to the next and that the softness in April is a one-off. In fact, tax receipts do demonstrate that April was a much softer month than the prior 2 and in fact resembles January. So far, May is tracking the strongest this year. Thus, we can reasonably conclude April’s softness is more a reflection of tax payments resulting in withdrawn liquidity than anything else, and it seems to be reversing for May.