I hope everyone is having a nice weekend. Last week had significant amount of data and the theme is tightening. The economy is growing well above its capacity, as evidenced by the across the board strength in NFP. CPI had something for everyone, but I think celebrations are deeply misplaced after going through the details. Meanwhile, markets have moved to their own tune of late, which tightened FCI materially this week. Is it over, or just beginning?

In terms of data this week, we have the weekly ADP on Tuesday. Wednesday we have MBS apps (watch for a surge this week), building permits, housing starts and durable goods, Redbook and industrial production. Thursday we have claims, trade balance, Philly Fed and Pending Home sales. Friday we have GDP as well as personal income/spending, core PCE (December), S&P PMIs, New Home Sales, and UMICH.

In other economies, we have NZD PMIs and Japan GDP today, Canada CPI Tuesday, RBNZ tuesday night, AUD employment Wednesday night and Japan machinery orders, and AUD and Japan PMIs Thursday night.

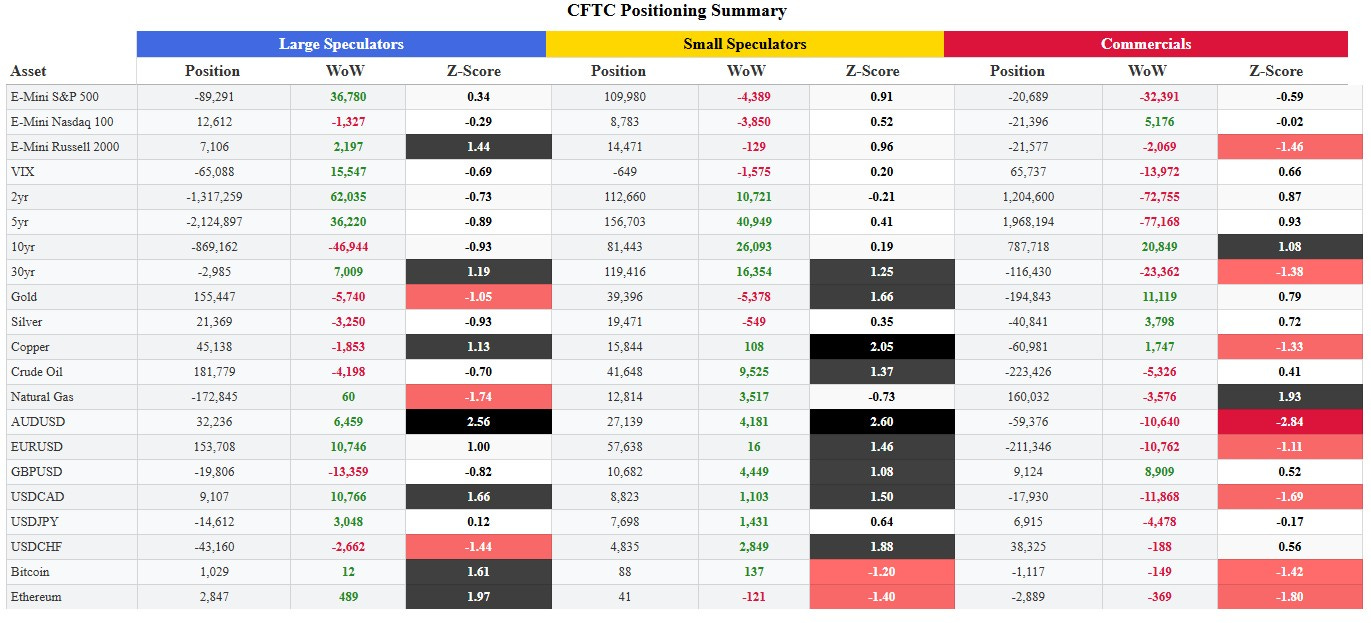

Updated positioning summary is below.

Prior work we will discuss in this note includes:

There is an enormous amount to unpack this week, so let’s dig in.

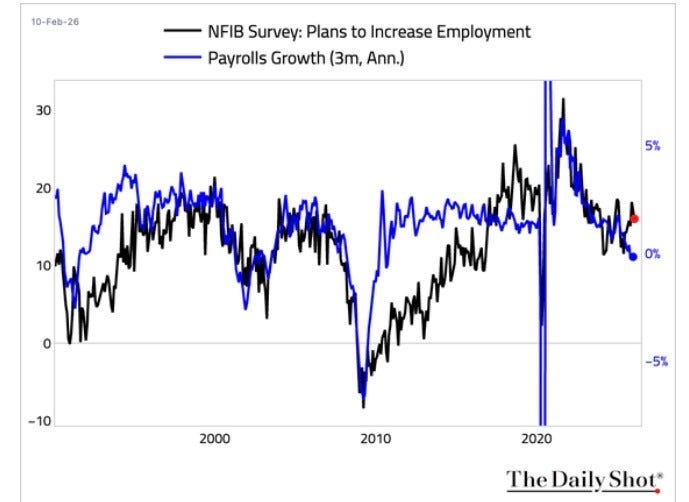

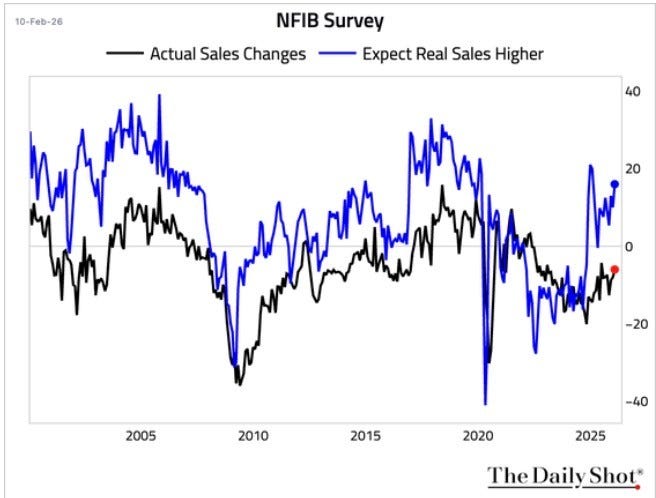

The first data we received was one I always look closely at, the NFIB Small business optimism survey. While little changed this month on the headline, the components tell the story. Hiring plans continue to point to an improvement in NFP ahead. Pricing plans continue to point to higher inflation ahead. Expectations for higher future sales had a notable pick up. All of these dynamics are more consistent with early than late cycle behavior, in line with the cyclical reacceleration theme I outlined in my macro outlook note.

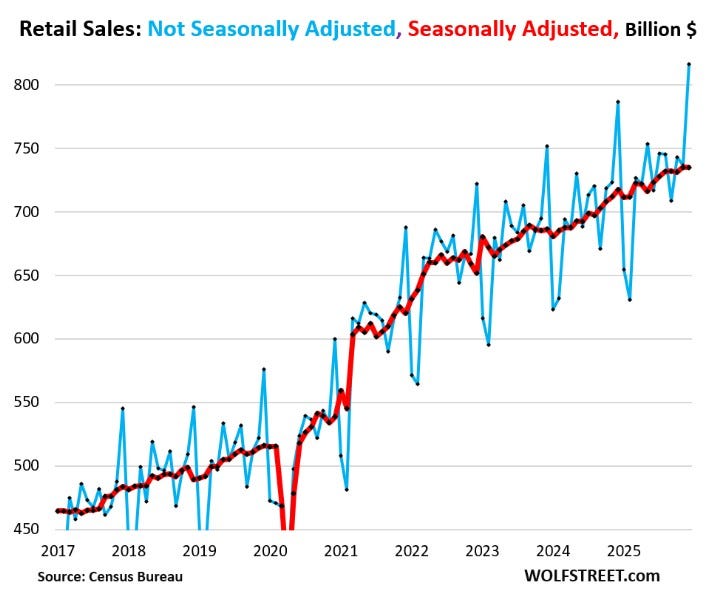

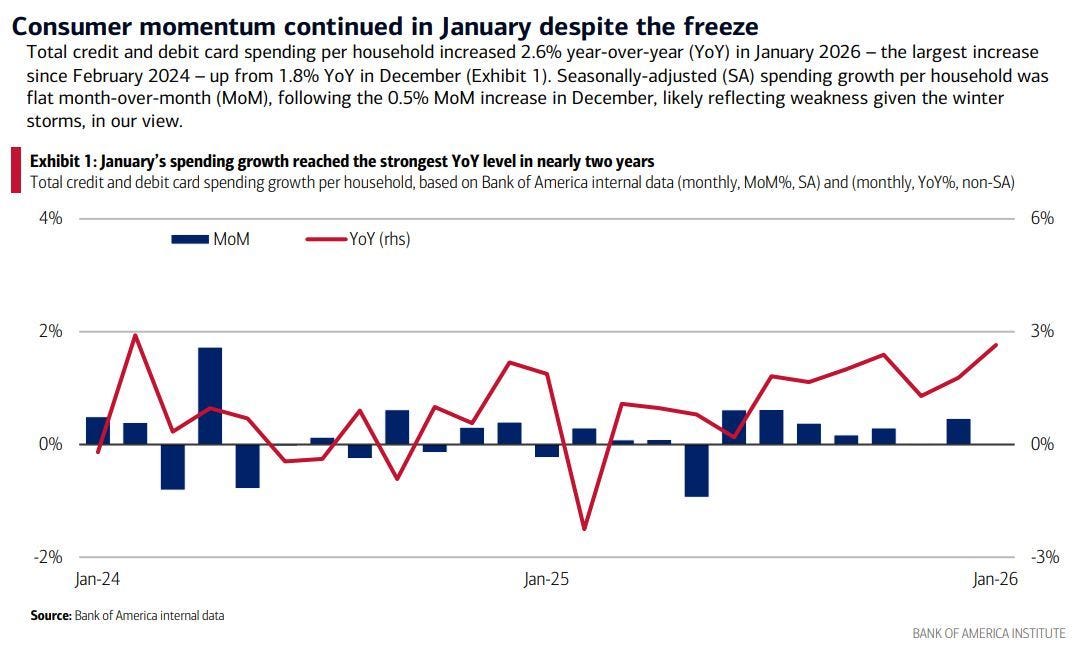

Retail sales was a disappointment and came in flat. Interestingly, we actually had larger than usual seasonal adjustments that may have contributed to that. Every December, the BEA uses seasonal adjustments to reduce the SA number, and then the opposite for January. This is normal, but look at the size of the adjustment vs prior years. The SA was in a pretty consistent range for a number of years, between 60-70BN and this year shot up by 18.8% relative to last year. It is beyond me to say if this is fair or not, but I am pointing out that NSA retail sales put in their best YoY reading in many months, and it was SA sales that were flat. This report stood out relative to other trackers, like Chicago Fed, NRF and Redbook. I think decent chance it gets revised up. BOFA card spending is accelerating to start the year.

Existing home sales were sharply negative on the month, and unwound a number of months of gains. Most people are attributing this to bad weather, which was historically cold and with heavy snowfall. Considering I didn’t leave my house for a few days in that period, I can imagine home shopping took a backseat for many.

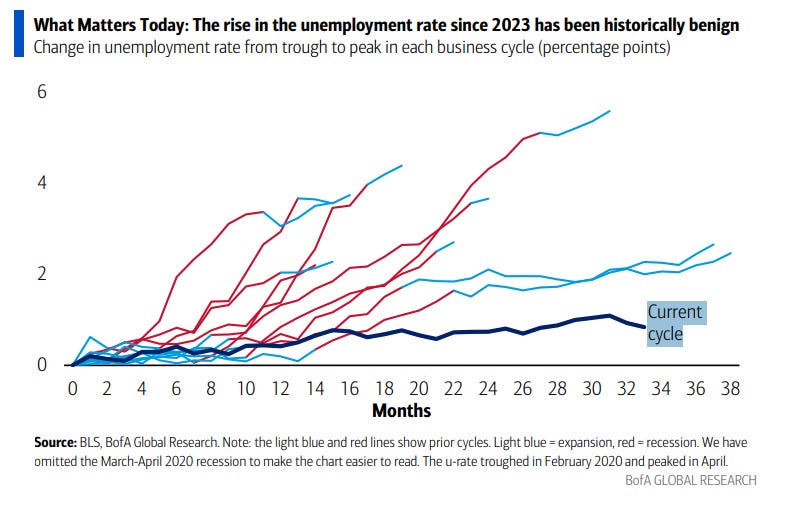

Next up was NFP. This was a blockbuster report in every way I look at it. Not only is the labor market showing clear acceleration, but due to the supply dynamics I have been discussing for a year, it is tightening. Meanwhile, those worried about the labor market need to answer as to why this cycle is the mildest increase in unemployment of any ever and why that justifies more than 175 bps of rate cuts.