Weak(er) print. Roughly 75k below consensus, AHE much weaker than other wage metrics we have seen, UR ticks up to 3.9%. Nothing to point to that was hot or a counter argument to the weaker view. This will be viewed as Goldilocks for now.

That being said, it was not WEAK. So this makes things a bit complex. Is this a start of weakening? Or were we simply due to print a report below loftier expectations? Remains to be seen. So let’s think through that for a second because the implications for markets will vary substantially.

On the margin, this raises odds of cuts for this year and reduces the tail risk of hikes. But does that mean we put back 5 cuts? No, the Fed raised the bar for cuts and they will need WEAK (not weaker) jobs data and multiple soft inflation prints in a row. So, we should not get over our skis in pricing additional cuts. Additionally, since we are talking a weaker (not WEAK) print, the economy remains in expansion, which means if we loosen FCI too much, it can reinvigorate demand and bring back right tail risk very quickly. FCI has loosened since the FOMC meeting and really had not tightened much at all. So if SPX goes +5% from here and 10y goes to 4.25 or 4% in a quick fashion, we stimulate again.

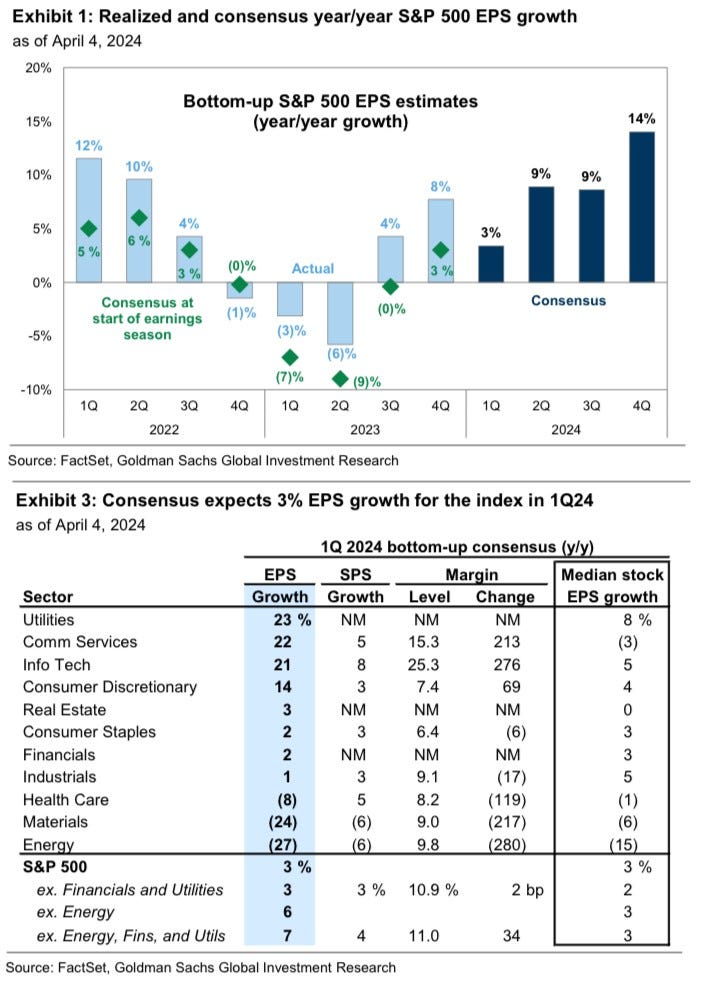

If this is the start of weakening in the economy, then how realistic are earnings expectations for this year? We roughly met Q1 expectations. We’re suddenly going to bounce in Q2-Q4 at a 10-15% rate? That is completely unrealistic.

So my high level thinking right now, which can change over the weekend, are as follows:

A weaker report doesn’t change my trajectory for the economy much as of now, but further weakness would.

Given #1, a material FCI loosening would provide another impulse to the economy. Again, this is why the Fed should not have been so dovish Wednesday even with this report. Speak hawkishly so that hopefully you don’t need to actually hike down the line again.

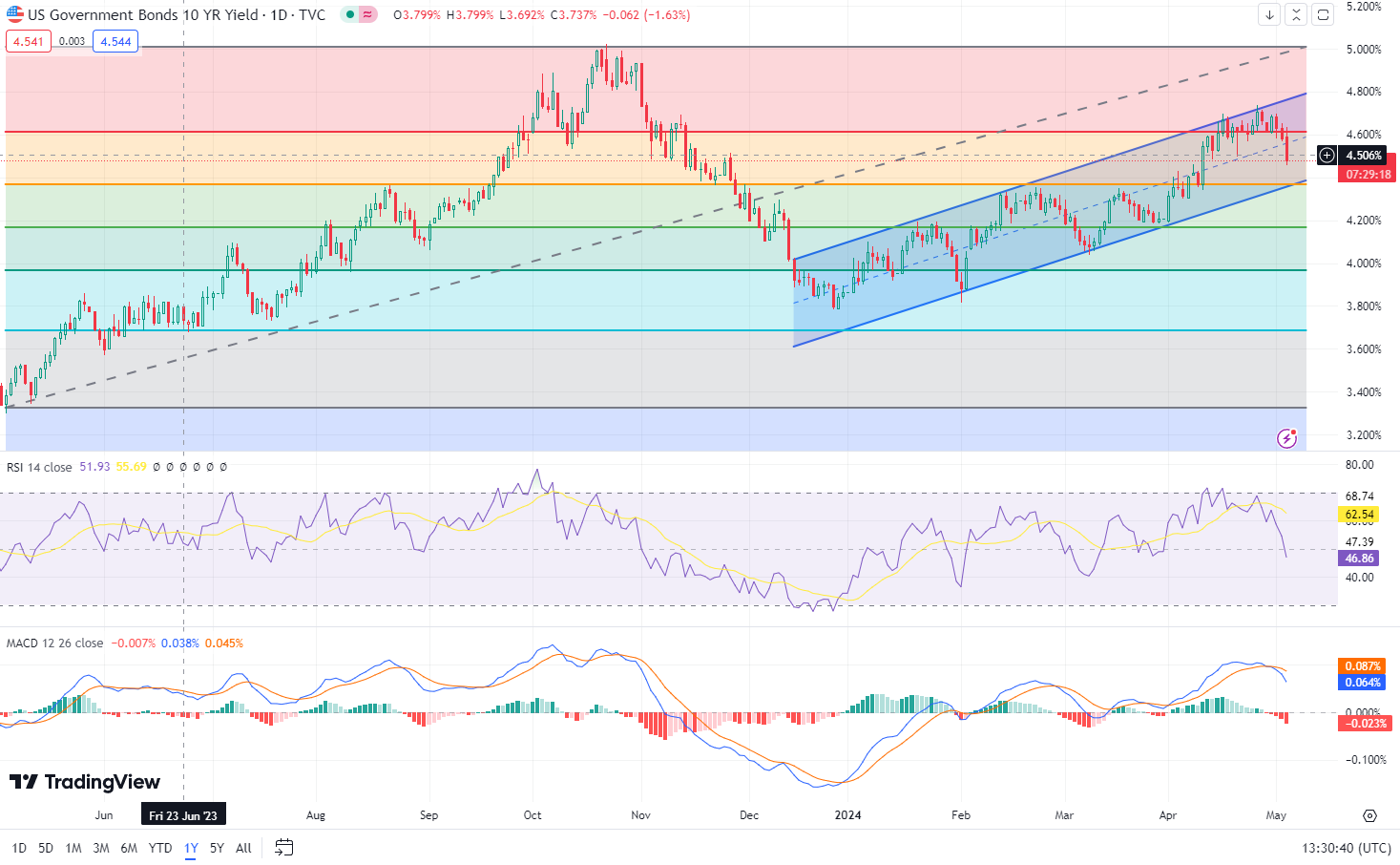

Besides a few days, stocks seem to have even worse risk vs. reward than before. If the economy is weakening, earnings will be much worse than expected, and we have not declined enough to provide value. If this is a blip in the road report, then bonds will eventually reverse this. Wouldn’t take much in data to do so.

So what’s my takeaway? I don’t want to react and buy bonds in the U.S. Supply remains massive, and I think there’s a decent chance this report may be viewed as a blip report, get revised higher, or just noise. With payrolls data, this is always a possibility.

Buy bonds in other markets that have had their rates dragged higher by the U.S. bond market.

Germany 2y: 2.40 → 2.90% this year despite weak economy

Canada 2y: 3.92 → 4.33% this year despite weak economy

You concentrate your longs there as these economies won’t need to look at cutting under pressure while their currencies collapse but they have the greenlight to cut. In FX, we will still get divergence, but softer dollar has legs for now. Buy equity markets outside the US.

I own Germany 10y (yes I know I said 2y but I think anywhere is fine), and I own CRAZ25. I am out of US rates trades for now, and will wait for better levels to short as I do not think the expansion is dead yet by a long shot. Notice that Copper bounced 1.5% off a soft(er) NFP print. Maybe that is a signal.

Any further thoughts now that ISM services have come in below at 49.4 and prices paid at 3-month high of 59.2?