Quick Data Reaction

Nothing really material to note, but in an otherwise quiet day, here goes.

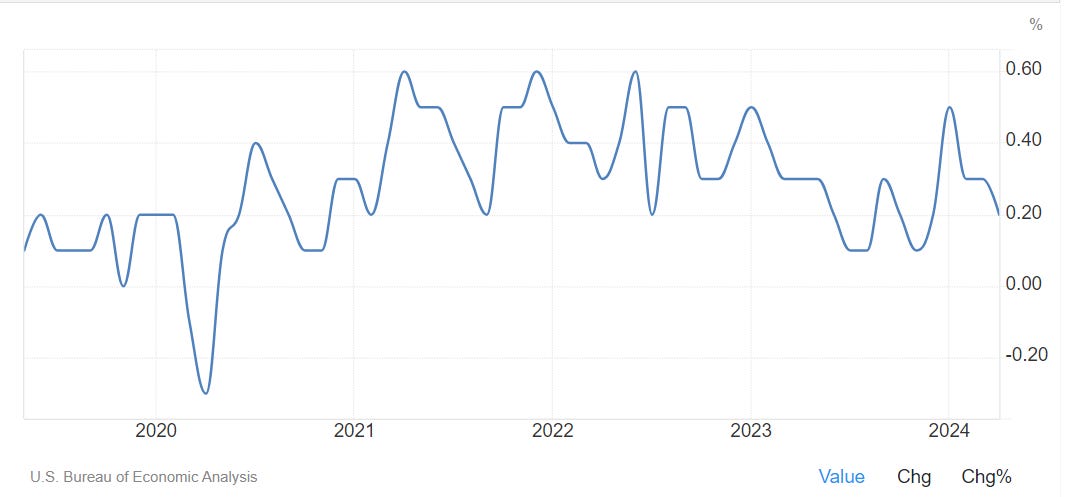

Core PCE prints 0.25%, which annualizes to 3%. Remember, Core CPI is trending at around 3.5-3.6%, and so if we look at core PCE, it is a less stable trend but also seems coalesced around 0.25%. We can celebrate or panic over little nuances of the data release, but we’re missing the plot.

The plot remains: 27 months from first hike, 11 months from last hike. GDP remains above potential, inflation (however you measure it) remains sticky above target, job growth averaging 250k/month. That is not restrictive, but won’t beat a dead horse here.

Personal income in line, spending a touch light. This is generally consistent with the rest of April data. I covered this before, but I believe tax payments caused a liquidity withdrawal and a softer month. I expect hotter May data.

Elsewhere, Eurozone core CPI printed 2.9% versus 2.7%, complicating the ECB’s messaging next week. I will have more to say in the weekly preview.

Canada printed weaker GDP, 1.7% versus 2.2% and the MoM was 0%. The totality of data gives the BOC to cut without complications. Remains to be seen on their guidance, but they will cut.