La Maladie

Canada's Growing Debt Problem

I discussed the outlook for Canada on the Market Huddle Podcast with Kevin Muir last Friday. The below is a deep dive into the ugly debt situation in Canada and its likely consequences.

The latest budget from the government of Canada is horrifically bad. It proposes substantial new spending at a time when deficits are already bloated and unproductive. To finance the larger deficit, the government is proposing raising capital gains taxes on higher income groups, which disincentivizes capital formation and investment. It is not just the government debt load that is a problem, Canada has elevated debt across all aspects of society, including the corporate and household sectors. As more and more income goes towards debt servicing, productivity declines. Productivity has already declined from the 1.8% pace from 1980-2000 to a 0.8% pace from 2015-2022. Thus, policies that involve more deficit spending and disincentivize investment are very poorly designed.

The federal government entered the COVID period with one of the healthiest debt situations among G-7 countries, but deficit spending since then has squandered its good standing. Interest payments as a % of government revenues have increased from 7.9% to over 10% in a year. While not at outright troublesome levels yet, it does not leave the government with substantial room to respond to economic weakness.

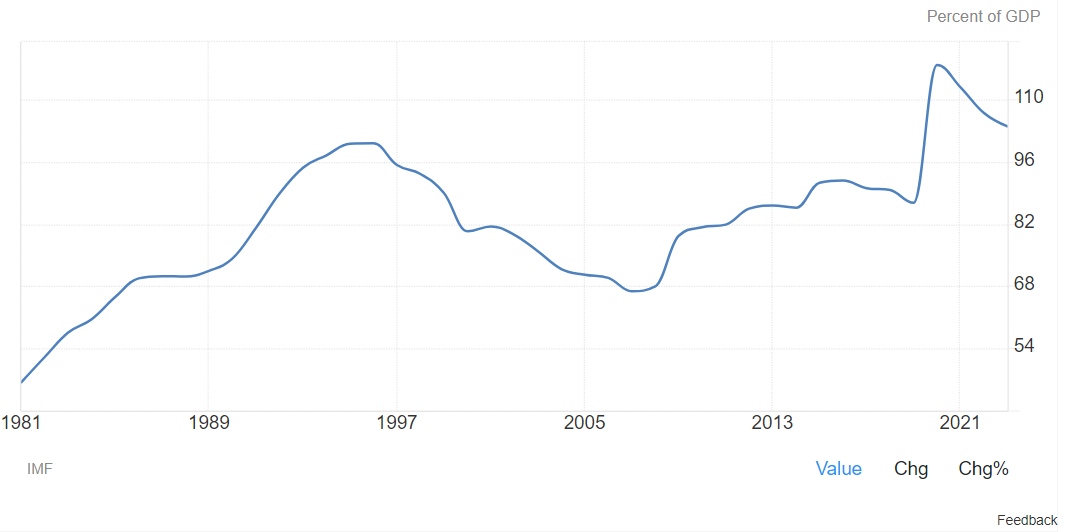

The corporate sector is amongst the most levered in major economies in the world, with substantially higher interest costs relative to disposable income than peer countries. The more that is spent on interest costs, the less is able to be spent on investments that can improve productivity and ultimately profitability.