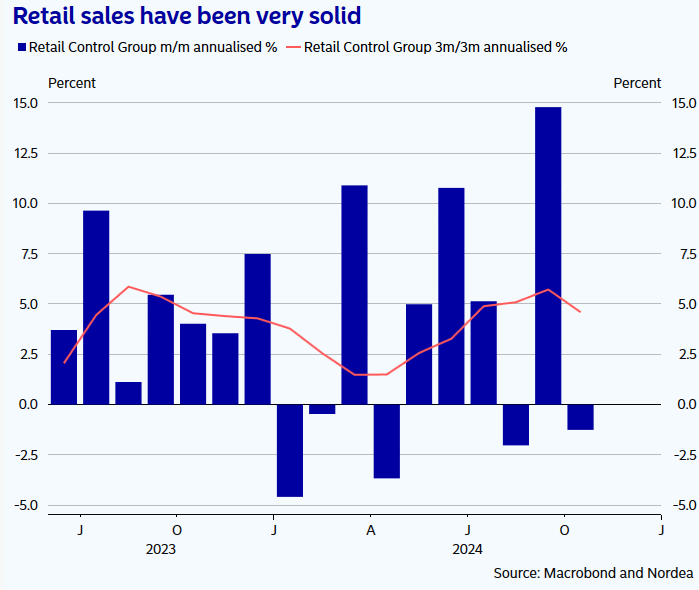

The highlight of the morning is the retail sales print.

Headline comes in at 0.4% versus 0.3% expected. However, the bigger story was the prior month being revised from 0.4 to 0.8%. This brings YoY from 2% to 2.8%.

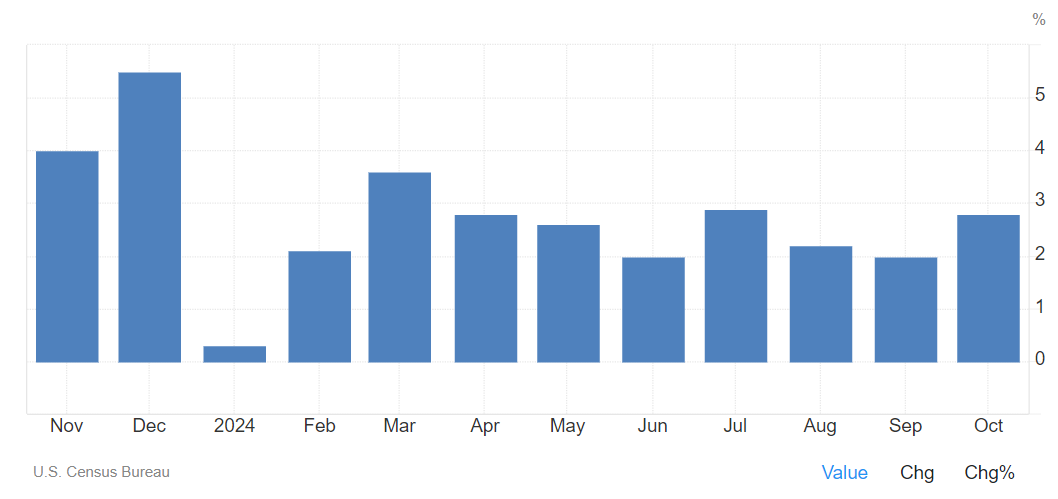

Control group was only 0.1%, which may have been hurricane impacted. Again, prior month sharply revised higher to 1.2%. Control group now looks like the below.

In terms of breakdown:

-auto sales had a huge month at 1.6%.

-Furniture sales down 1.3%, which offsets prior month.

-Electronics had a huge month at 2.3%, reversing prior month.

-Clothing was down -0.2%, which makes the point that the apparel number in CPI looks anomalous and should adjust sharply higher.

Given the hurricanes, it’s reasonable to expect a very large number next month. While this is partly covered by insurance premiums, so not a full GDP bump, but there will be car replacements, furniture, electronics that need to be bought for those that had unfortunate damage to their belongings.

There were some other notable data points.

-Import prices 0.3% versus -0.1% expected.

-Export prices 0.8% versus -0.1% expected.

More inflation basically.

And onto fringe data that is not usually a big focus, but look at the NY Manufacturing index, which is possibly another sign that the goods economy is picking up.

In terms of trading, I have taken off my SOFR Z5 outright short at 96.08. I first sold it at 97.18, and covered it a few times and sold each time after a few bps rally, which means I made more than 110 bps on this.

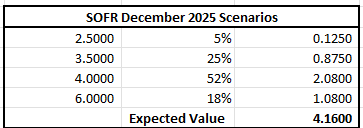

I have updated my scenario analysis after digesting the election result. I expect a boost to the economy as discussed, so I have reduced my recession risk scenario to 5% and my soft landing scenario to 25%. I modestly increased my base case scenario from 50 to 52% (it is already playing out), but I raised my second wave scenario to 18%.

To be clear, when I say second wave, it doesn’t necessarily mean 8% CPI. A move above 4% would be a notable enough reacceleration that I think the Fed would need to reverse cuts delivered, which would take us back to 5.375%, and I think the Trump agenda may even require higher rates if tariffs are implemented first before supply side policies like tax cuts are. Given the strong starting point of the economy, it would quickly raise inflation before any supply side improvements can offset that to some degree. The Fed would respond.

Either way, given that any bad data point can result in a 25 bps rally in Z5 to price in more cuts, it is not asymmetric to hold a large futures short position. As such, since I still think we need to price higher, I instead converted the position to an options trade, and bought the December 2025 95/94 put spread for 0.075, for a 13:1 potential payout by next year.

I have put ladders on for Z5 and M5, so if rates stay around these levels or only move higher by 25 bps or so, I do very well. If they hike, I do very well too but would take the ladders off. I have a lot of scenarios covered for the next year.