Been awhile since I did one of these.

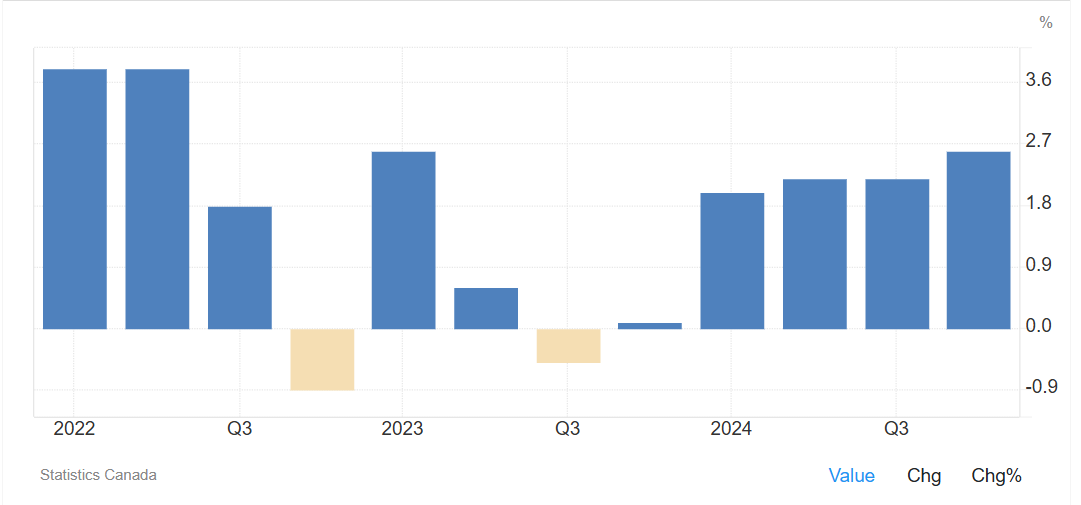

First, let’s look at Canada’s GDP report. It came in at 2.6%, well above the 1.9% consensus and above last quarter of 2.2%. After two solid job reports, retail sales which was strong and now GDP, BOC is done cutting unless trade wars are implemented. We are down to the deadline on it.

The first thing that I expected today was a narrower trade deficit. Nope. This is a massive two month widening, which means imports > exports. The U.S. economy is an import economy and this means demand is very strong, with some definite frontloading but this will certainly lead to a stronger ISM manufacturing print.

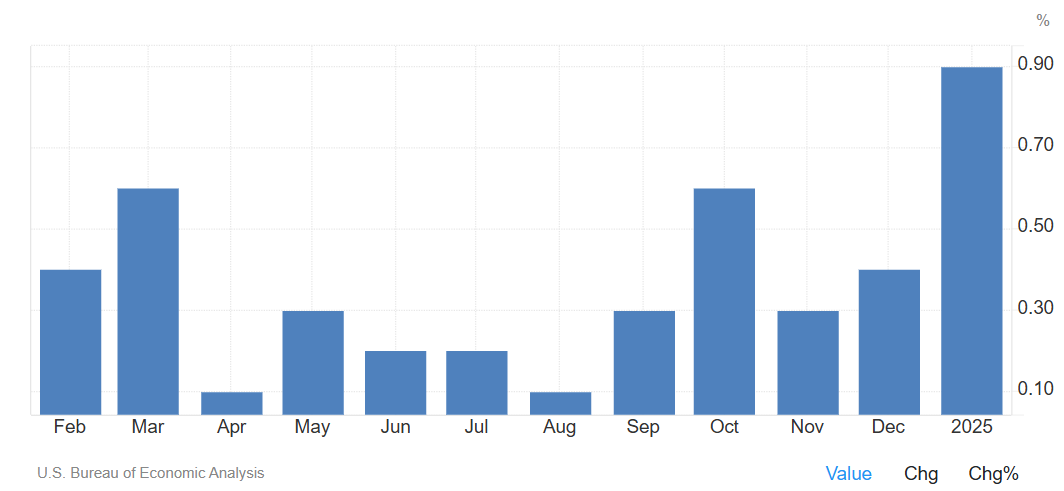

Core PCE comes in at 0.3%, in line with expectations. Given we had CPI & PPI, this is not very interesting to me.

Personal income was an enormous 0.9%. Hard to be downbeat on the consumer when that is the case.

Details:

-Wages and salaries grew at 0.44%, a very solid wage number and above recent readings. Last month was 0.4%.

-Rental income was massive, think of landlords renting their homes. 1.384% MoM. Just massive. What does this imply for shelter? It seems rents are increasing, not decreasing.

-Income on assets (interest and dividends) grew 1% in the month. Will certainly not be as wonderful for February.

-1.8% transfer receipts. Looks like this is social security driven, the annual bump.

=Disposable income grew 0.88% MoM, or 10.5% annualized. Massive!

Spending: Down 0.2% on the month after 0.8%. Clearly some giveback from that huge sending in December, but also we saw retail sales were held back by weather. This is less bad than retail sales was and I think that is a good sign as this is a more comprehensive spending report.

-Spending on services was strong at 0.33% MoM. Remember, this is not in retail sales.

-Goods was softer, in line with retail sales at -1.2% on the month. Keep in mind the trade data above, which means businesses bought input goods but they haven’t been consumed yet. So if anything, should be better here going forward. Of course, counter argument could be the frontloading of inventory ahead of a demand collapse, if it happened, would lead to bloated inventories. Let’s keep an open mind.

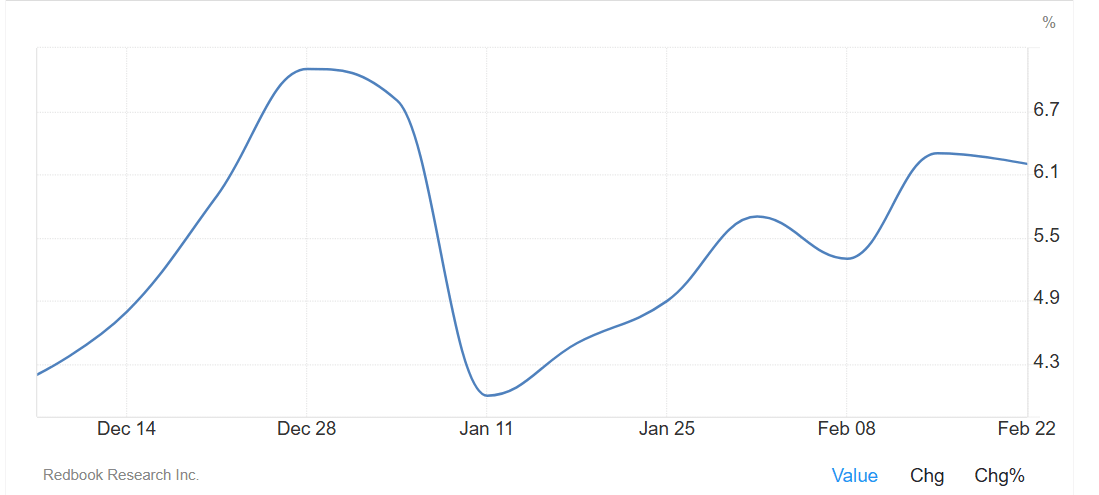

As a result of the spending being negative and huge incomes, the savings rate rose to 4.6%. Still quite low, but we do not want to see this continue. So, we need to see spending improve next month which I think it will. Why do I think that? Redbook tracking, which did show a sharp fall in early January as weather was very cold, then bounced towards end of month but was nicely up all of February.

All eyes on NFP next week and CPI the week after along with retail sales. I think they will all be strong and this growth scare will have passed.