Hi everyone. I hope y’all had a good week.

I will be travelling this weekend and so there will not be a weekly note on Sunday.

I plan to release 3 notes next week:

Crypto Update. There have been no signals the last two weeks, but I will do a deep dive on Tuesday.

Canada Update. Latest data there requires an update to my thought process for this theme.

The Pipeline. A look at how supply chain pressures work their way through the system.

It should be a busy week with jobs data and NFP, and the endless war headlines.

I will do a data recap below of today’s data.

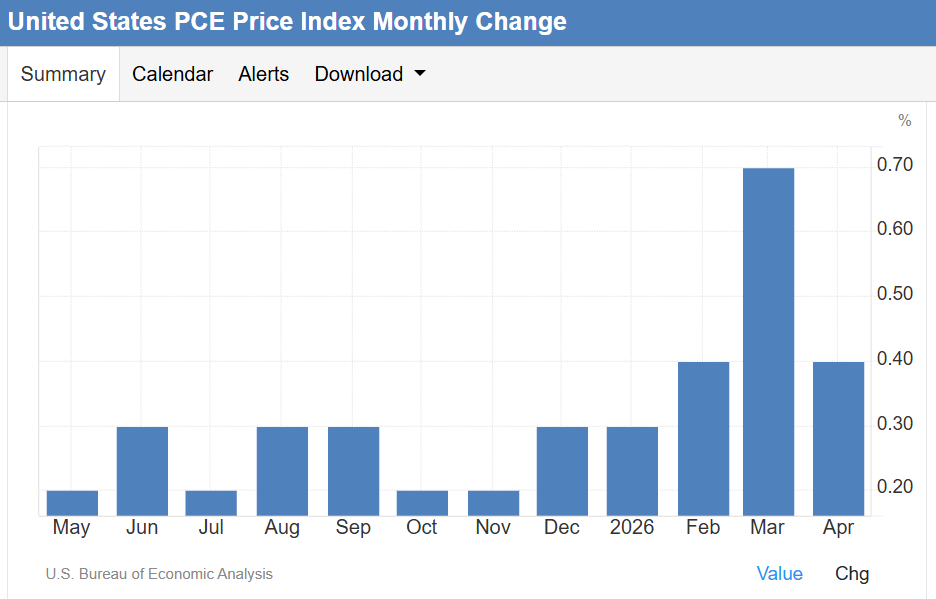

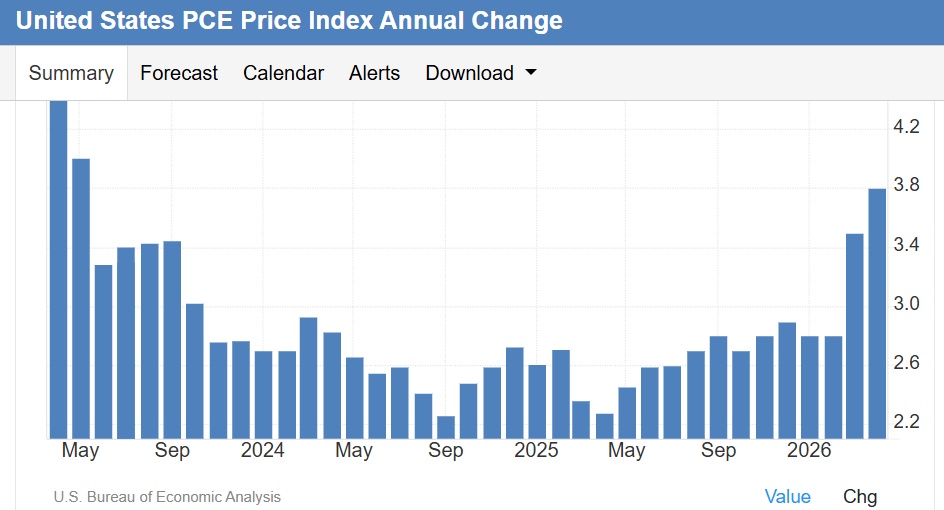

Headline PCE comes in at 0.4 versus 0.5% expected. YoY is lifted to 3.8%, highest since May 2023.

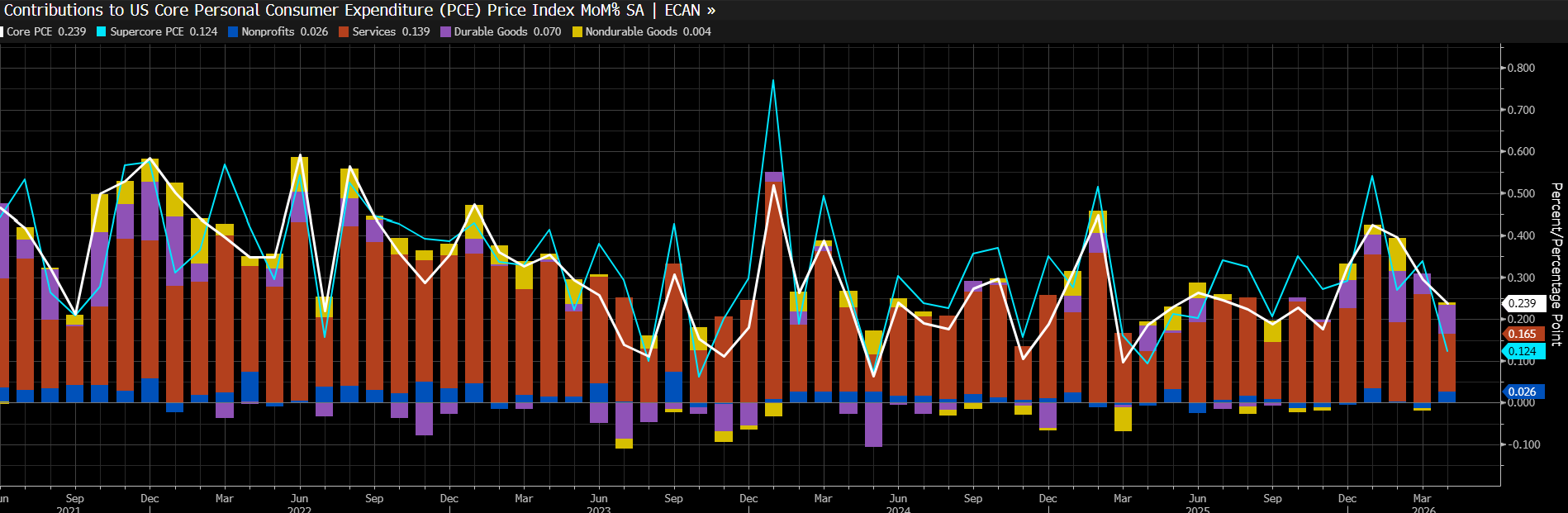

Core PCE comes in 0.239, so rounds down to 0.2. Pretty close to 0.25 which would be 0.3 and consensus. If you look at the breakdown, it is due to services, which came in at 0.139 MoM versus 0.2-0.3 recent run rate. Supercore came in much lighter than usual and is the suspect.

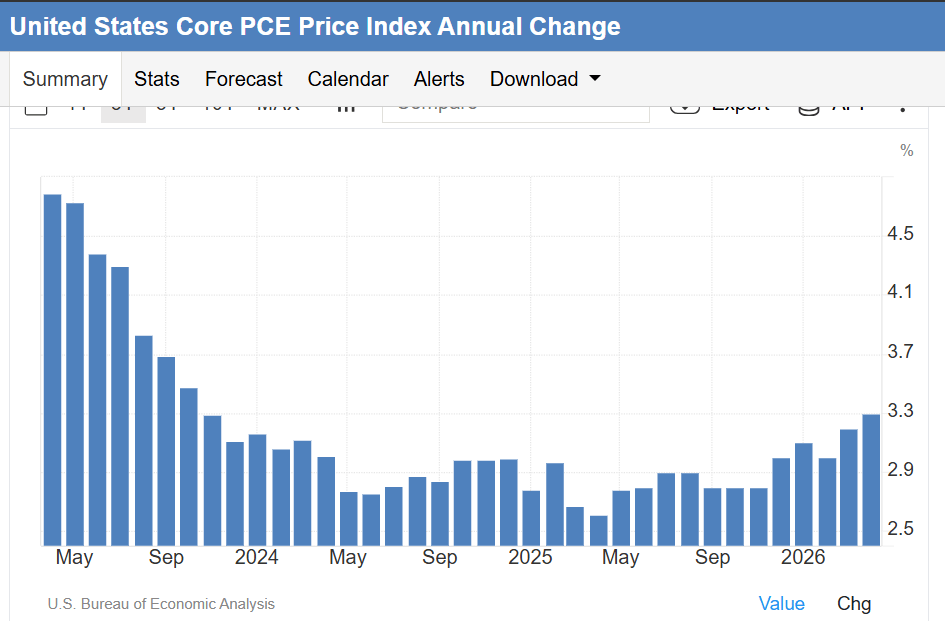

In spite of this weak print, Core PCE is 3.3% YoY, highest since November 2023.

The really shocking part of this report is the personal spending data, which came in at 0. Private wages were at 0.2% versus the 0.3-0.4% typical run rate. It’s also lower than tax receipts which tracked 0.35% MoM range. Looking into this closely has me less concerned. The big drivers of this miss are two things:

Dividend income was 0.1 from 0.7 prior month. Given how well stocks did, this does not seem to be something to be worried about and I would expect it to bounce back.

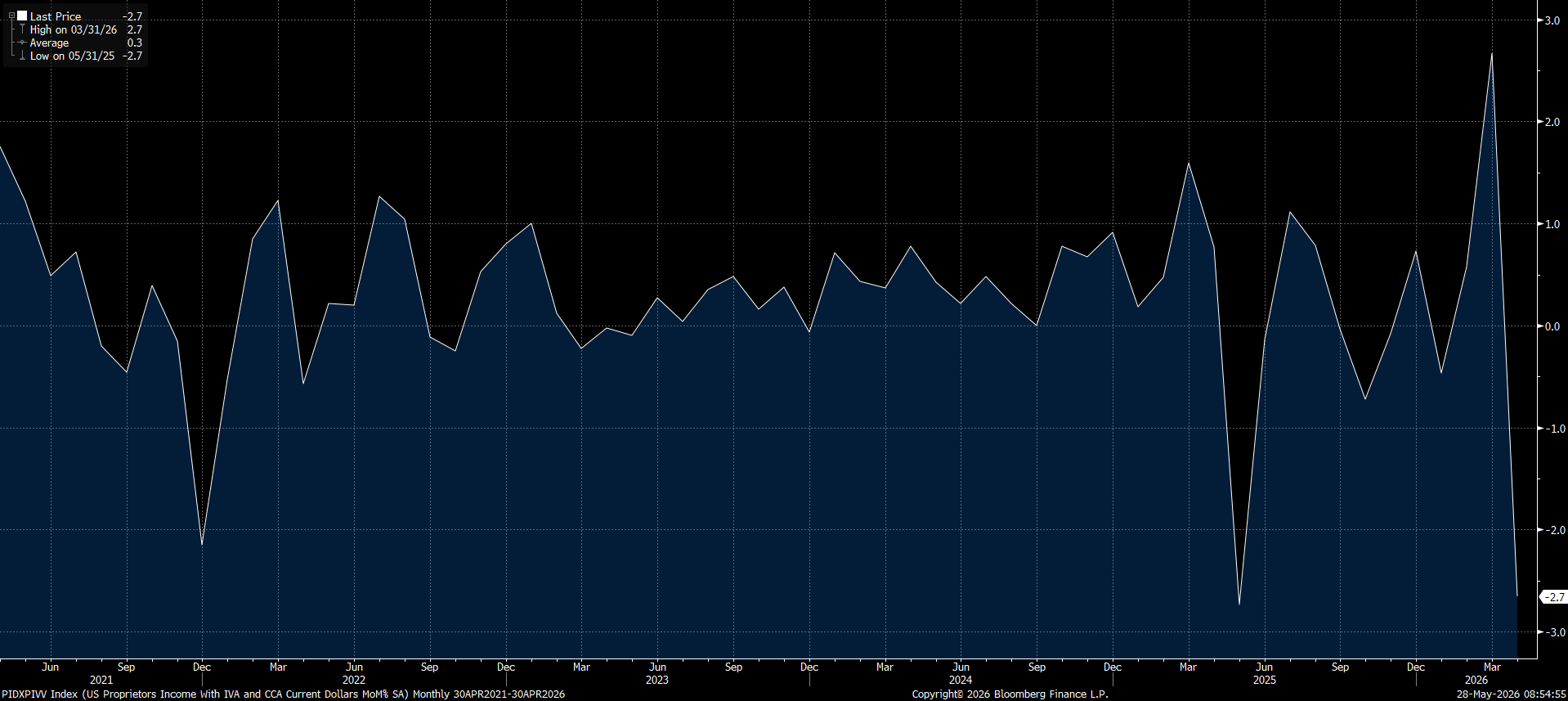

Proprietary income with inventory valuation and capital adjustments. If we look closely, it is farm income. It is beyond me to know what this actually is, but it went from 101.8 to -54.8, an enormous swing. The second chart below shows the entire proprietary income category monthly print and we can see this looks anomalous. We had a sharp print like this in December 2021, and May 2025 but this doesn’t look like something we should be too focused on for health of the economy.

Spending came in at expectations at 0.5%. Strong breakdown between services and goods. Goods is lighter than prior two months but other than that would be strongest since June 2025. Breakdown of goods shows it was dragged down by auto sales, which makes sense in the inflationary context.

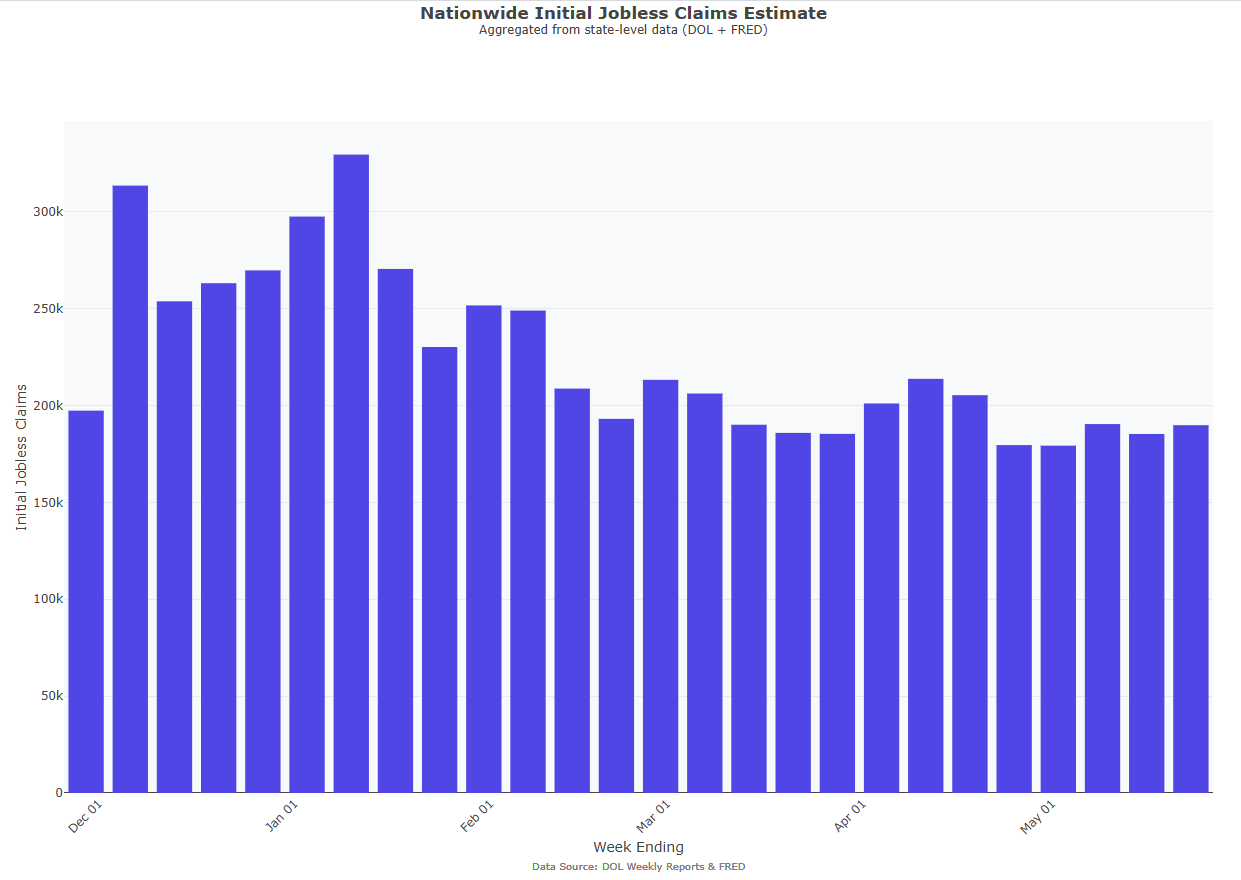

Jobless claims remain historically low. I always look at NSA and it came in at 189k, in line with recent run rates.

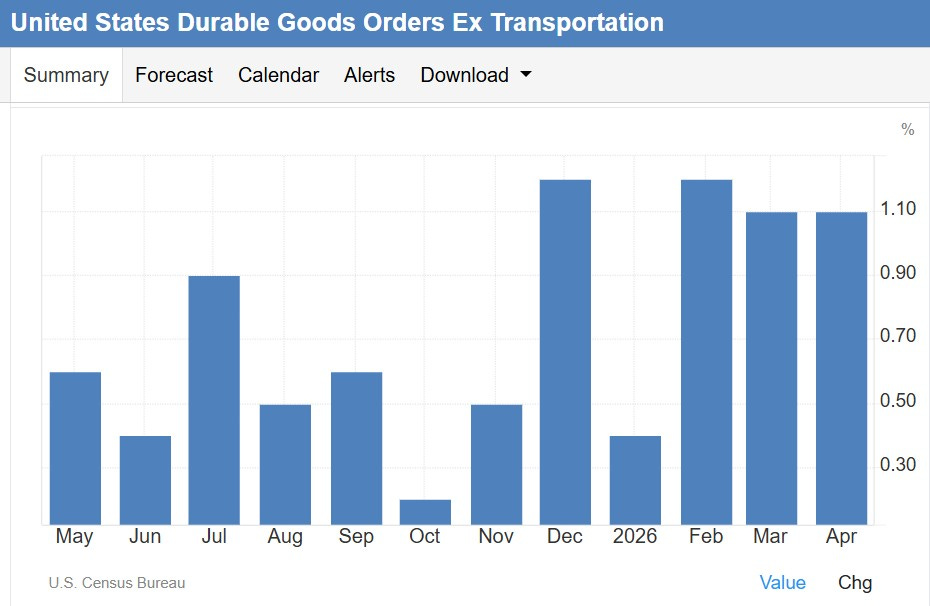

Core durable goods keep exploding higher, printing another 1.1% month, well above expectations of 0.5%.

Is is stupid of me to ask you for specific high conviction trades?

Appreciate these quick little recaps!