I hope everyone is enjoying their July 4th weekend, hopefully with some sun and BBQ.

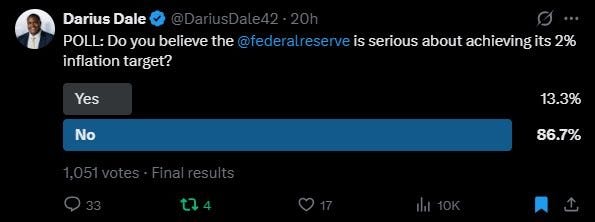

The labor report had something for everyone, with a lot of noise. Most of all, it will give the Fed comfort that they don’t need to urgently hike. That means passive easing continues, and raises the amount they will eventually need to do. They remain unserious, but don’t just take my word for it.

In terms of data, tomorrow we get ISM Services. On Tuesday we get LMI, Trade Balance, Redbook and ADP weekly. Wednesday has MBS apps and used car prices. Thursday we will get claims and existing home sales. Friday is empty but there is Canada’s employment report.

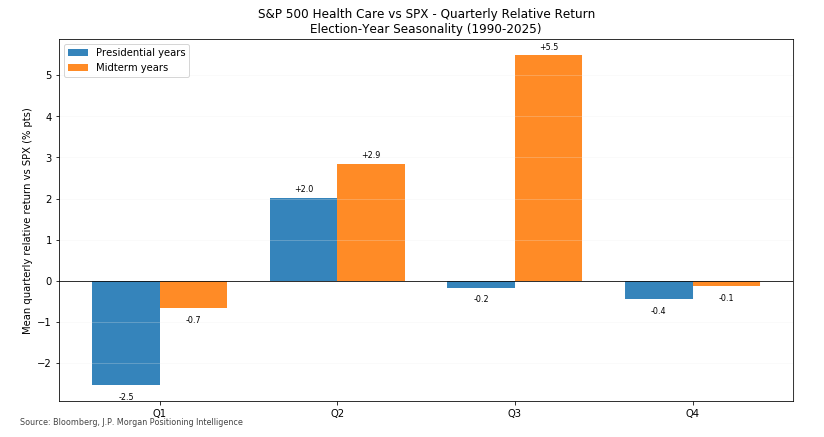

If you have not had a chance to read, check out my latest AI note, The Next Phase For AI with a focus on healthcare. It had a very strong week and enters a historically bullish period from here as well.

Let’s get into it.