Ahead of NFP, the labor markets remain at a turning point. Is this normalization? A stalling in demand that reinvigorates after the election uncertainty passes? A precursor to layoffs picking up and ultimately a recession? That is what is being debated by economists and markets alike. Ultimately, the data will tell us, but in the meantime we can do our best analytical work to guide us.

This note is about whether we can develop a model that provides a leading indicator for permanent layoffs, the type that are most prevalent in recessions. We will get to the model specifications and conclusions in a bit, but first let’s take stock.

In the Week Ahead - Sept 9-13, I recapped the prior NFP report. Let’s look at a few tidbits from that report.

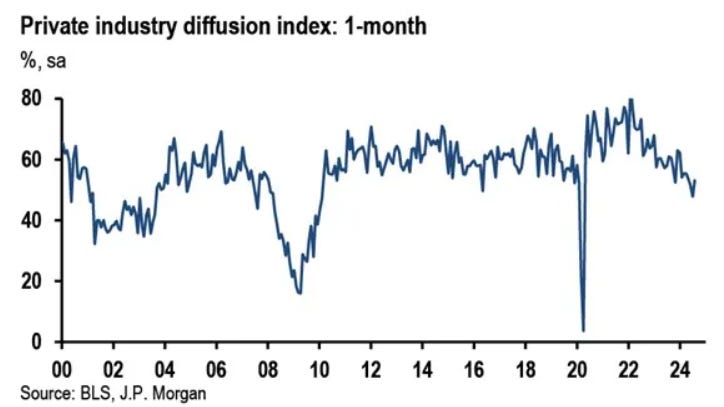

Headline job growth has slowed to roughly the replacement rate of the population on a 3 month rolling basis. More concerning is that private sector job gains are increasingly narrow, as shown by the fall in breadth.

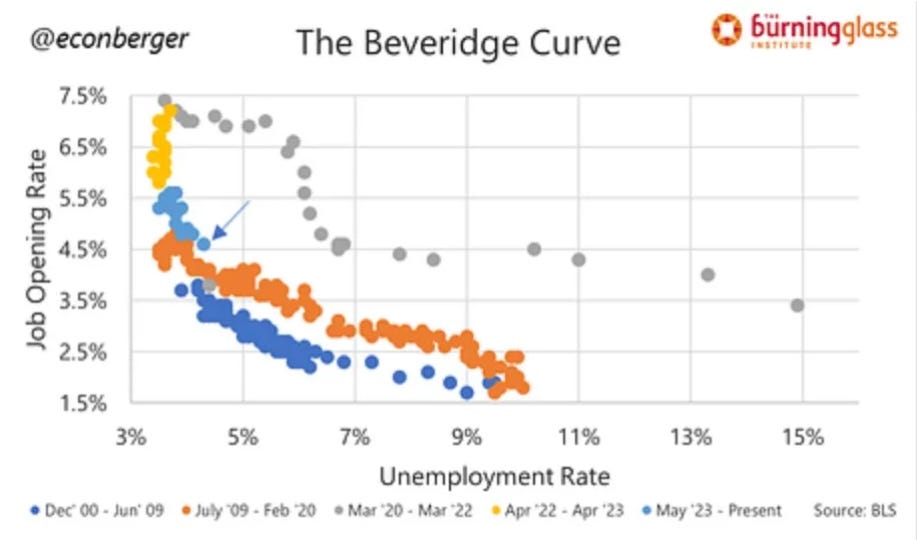

The Beveridge curve is now a mainstream topic of discussion, and the fear is falling openings would put us at a place where the unemployment can rise rapidly as layoffs would be next.